Farm tax ratio recommendations will help PEC agriculture: Thompson

Administrator | Nov 15, 2017 | Comments 17

John Thompson

John Thompson, president of the Prince Edward Federation of Agriculture, is returning to council to address the Farm Tax Ratio.

His detailed deputation illustrates the effect of the tax shift on a typical family farm and notes implementing tax ratio recommendations would be positive for retention and growth of agriculture and associated businesses.

His deputation:

Last year many Ontario farmers were shocked by the 2016 MPAC assessments that saw farmland taxable values increase by an average of 65 per cent over the four-year period, 2016 to 2020. The farmers of Prince Edward were much more affected than most, as our average assessments were up 112 per cent.

These increases have not resulted in a lowering of the tax rate as the farm tax class made up just 1.6 per cent of County tax revenue in 2016 (as referenced on the staff report of Jan 12, 2017). The province allows the farmland property taxes to be set at up to 25 per cent of the residential rate and council decided to continue with the maximum allowed for 2017, resulting in average farmland tax increases of over 25 per cent this year. This tax shift onto farmland also gave a small bonus to the residential tax class, resulting in it reducing from 90.17 per cent of County revenue to 90.15 per cent, a difference of just 0.02 per cent.

While MPAC is responsible for farmland assessments, the farm tax ratio is the responsibility of each municipality. As this ratio is capped but flexible, MPAC is not responsible for the tax increases which farmers have begun to experience.

The two most widely held principles of property tax fairness are (a), the ability to pay principle and (b), the benefit principle. The ability to pay principle does not justify major tax increases since farm commodity prices continue to float in the range of the early 1970’s and the commodity boom that peaked in 2012 seems like a distant memory.

Farmers are price takers in the market, not price setters. The sharp increase in farmland assessments and resulting tax increases mean that farmers are paying substantially higher taxes while continuing to consume the same level of services.

The Ontario Federation of Agriculture did some calculations for us last year. These appear on the January staff report. In order to keep the farm portion as the same 1.5 per cent to 1.6 per cent of County revenue, the farm tax ratio would need to reduce to 20%, 17%, 14% and 13% respectively over the four-year period.

With this scenario, the farmland tax would increase only at the same percentage as residential and the share of revenue from residential would increase from 90.2 per cent to only 90.5 per cent. The farm residence would continue to pay the residential rate as always.

Keeping the farm tax ratio at 25 per cent ratio for the four years would mean that the residential share of revenue would decrease from 90.2 per cent to 89.2 per cent and the farm share would increase from 1.6 per cent to 2.9 per cent, an astonishing increase of 80 per cent as more taxation shifts to farmland.

As reductions in the ratio to 13 per cent over the four-year period would be perceived as excessive, we are continuing to ask that the default rate be reduced to 20 per cent going forward. This would have the effect of levelling the farmland taxes for 2018 followed by 2019 being 20 per cent higher and 2020 would be 40 per cent higher than 2016, a major increase by any standard. This is a realistic proposal on our part to make a reasonable compromise.

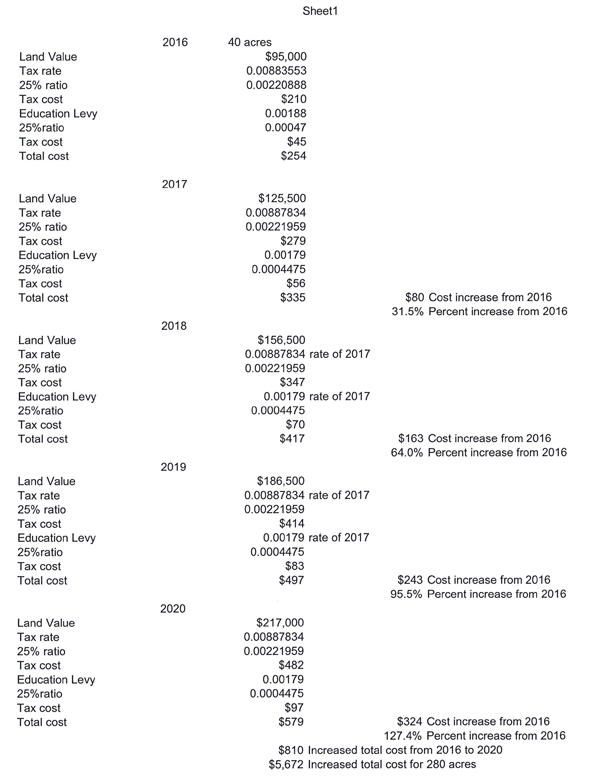

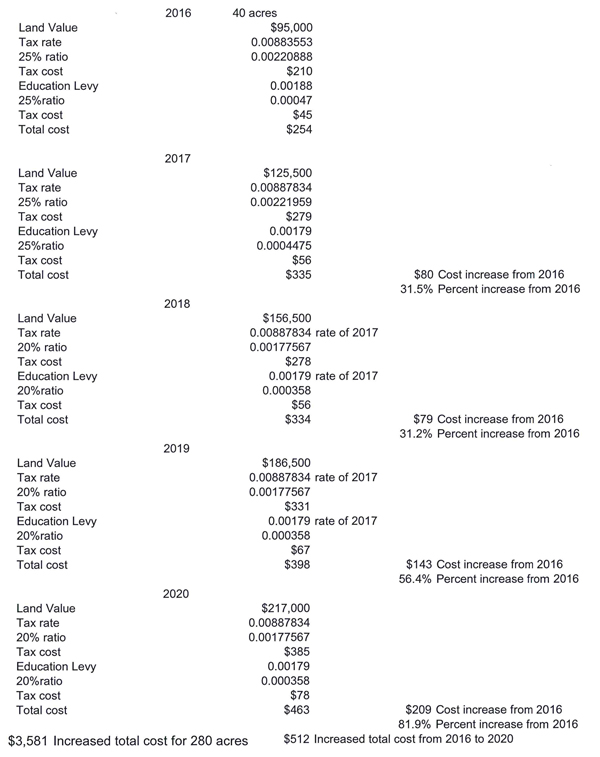

It has been suggested to me that it could be helpful to use dollar amounts rather than percentages to illustrate the effect of the tax shift on a typical family farm. In so doing, I was able to use a 40-acre farmland tax bill which had no residence or farm buildings and extrapolate the numbers to 280 acres, which is the average farm size shown in 2011 statistics. The farmland tax would have been $1778 in 2016 and would rise to $4053 in four years with the 25 per cent ratio for an accumulated tax increase of $5672. With the 20 per cent ratio it would have risen to $3241 for a four-year accumulated increase of $3581, still a considerable increase to farmers and a small tax shift bonus to the residential tax base.

(Spreadsheet below).

Precedent may be the main argument against lowering the ratio but we see this argument as disingenuous. There are no comparable tax classes to come forward for reduction. The residential ratio is set as 1.00 and small classes measure against that. As residential tax makes up 90 per cent of tax revenue, a reduction in the farm tax ratio makes very little difference as it is absorbed by such a large base.

Another argument that may come up is that the residential class may be facing large assessment increases in the next round. We see this as flawed as well, as a large and consistent increase would result in a reduction in the tax rate which is needed to balance the budget. Consider a fictional world where residential makes up 100 per cent of the revenue and the assessments go up 100 per cent. There would be no resulting tax increase as the tax rate to balance the budget would decline by half. Now review the concept with 90 per cent of the taxes coming from residential and realize that a major assessment increase would not have much effect on the individual taxes.

Agriculture is a very major component of our County economy, in the range of $100 million per year. Statistics show over 80 per cent of farm revenue going to pay operating expenses. Capital expenses, principal payments, personal taxes, community donations and family living are additional to this.

County residents highly value a local and domestic food supply as well as the enjoyment of our rural fabric and landscape. With agriculture being the back-bone of the County culture and economy, we should do everything possible to protect the family farms of the County. Implementing these tax ratio recommendations would be a positive action for the retention and growth of agriculture and associated businesses.

Filed Under: Local News

About the Author:

How can this be back for any kind of debate? We have folks paying more for water than hydro! A former Councillor brings this forward again. Council needs to stand up and say we have spoken on this issue, thank you.

no one gives the regular homeowner a break on their taxes so why should a farmer get a break

This Council has already debated ,spoke and ruled on this matter. Why is it back on the agenda?

Farming looks great from this side of the keyboard. Almost

every “tax break” described here is available to every taxpayer.Except the $750k exemption on capital gain.

farming is unique in that it requires virtually millions of dollars worth of capital investment to earn an income that perhaps some well paid teachers earn with ZERO risk.

What great benefits. I hope council are aware of this before they go and spend lots of time debating. I agree Dennis, you have to now question the purpose behind the request. What an enlightening post, thanks Chris.

Staff should be providing this information to Council. The capital gains advantages over other property owners is mammoth.

Chris – thank you for the information you have provided. It now makes me wonder what the purpose is behind this request to Council to lower farm taxes – and why aren’t the public being told this by politicians? Are they even aware of it?

Readers may be interested in knowing some interesting facts about taxation as it pertains to full-time farmers based on information from Intiuit and the Government of Canada.

The Ontario government administers a program called AgriStability designed to keep farms viable if they experience a large decline in their profit margin from drops in income.

AgriInvest helps farmers manage small income declines, and provides support for investments to mitigate risks or improve market income. Farmers make deposits to their AgriInvest account based on a percentage of net sales and are eligible for matching government contributions of up to $15,000 per year.

All the usual business expenses can be deducted from farm income including property taxes on the land, and business-use-of-home expenses (including a percentage of the property tax on the home) if it was used for business reasons. Farmers can claim the costs of: fertilizers, veterinary, medicine and breeding fees and fence repairs. Interest on loans and the amount of deductible premiums to the Crop Insurance Program are also claimable.

Each individual farm taxpayer is entitled to realize $750,000 of capital gains tax-free on qualifying farm property during their lifetime. Qualifying property includes real property and quota used in a farming business, as well as shares in a family farm corporation or an interest in a family farm partnership. Their dwelling is not subject to capital gains. In contrast, an individual selling a vacation home will pay roughly 25% of the gain in tax.

A farmer can transfer ownership of their assets to their spouse at cost, which means that no capital gains will be realized until the spouse disposes of the property.

A farmer can also transfer the ownership of capital property used in their farming business to their children at cost. Once again, no capital gains will be realized until the children sell the property.

Full time farmers have no limit on the amount of losses that are deductible. These can be deducted from income from all sources (n.b. not just farm income) – and carried back for three years or carried forward for up to 20 years.

From this it appears to me that farmers are well-served when it comes to taxation and government support and do not need County residential property owners to subsidize their property taxes.

Agreed.

The crux of this matter and of John Thompson’s complaint is the fact that they are getting richer by having the value of their property going up. This is not a hardship case he is talking about – but rather one of increased wealth that he says he can no longer afford. I am having a hard time supporting his concern. Where was he and the OFA when waterfront property owners were being driven off their land, or out of the family cottage, due to MPAC and huge property tax increases?

The weather does not only affect farming, it has ramifications on other sectors who do not all ask for tax reductions and if grain is not selling at the right price, maybe try and sell something else. If widgets don’t sell, then we don’t ask for a tax break, we change what we sell, or should we maybe ask that some of our tax hikes are moved elsewhere… I know, to the farming sector… that would again be fair wouldn’t it!

I see a lot of very well off farming operations. Their capital continues to grow as land values increase. This was rejected the first go around for good reason. It shouldn’t be back on the table.

Prime ag land can’t be severed for development. Unless of course you want a new OPP building which was permitted.

If you companies think farmers have it so good, why don’t you try it. Grain prices over the last few years are down and with the weather we have had the last few years we deserve at least a tax reduction.If you don’t like water and sewer rates move to the country and buy a farm and your troubles will be all over

This would be a reduction on the sort of prime agricultural land that is then severed off for a huge profit. A cool $7 million for 117 acres in Wellington, with 2017 taxes of only $857. Yes, let’s pass the bill to residential, seems fair!!

Here we go again, second time around perhaps better results. They want to shift their tax share to the residential taxpayer. No thanks. Just like I would like to shift a portion of the $200 per month insane water bill!

I think John Thompson needs to realize that every municipal taxpayer faces the same kind of increase that he does. This Current Value Assessment (and MPAC) was adopted under the Mike Harris government – a government that the OFA supported at the time. As a councillor, John Thompson supported IWTs and keeping council the same size – at 16 councillors. More recently, he is the inventor of the 14 councillors plan – which removed a representative from his own ward (Sophiasburgh) and ended up at the OMB! Sorry, I have no reason to accept his tax avoidance arguments – I hope our Council doesn’t either.